What are the key financial considerations when having a child?

Congratulations on having a baby – this represents one of the most consequential and life-changing events you may ever experience

There are many emotions to navigate as well as some financial considerations to keep in mind. For perspective, the average American family spends about $330,000 on raising a child to age 18, and of course, these expenses can be even higher given your choices around childcare, education, standard of living, extracurricular activities, travel, etc. (Source: Northwestern Mutual)

So, as you are having a child, here are 8 wealth management bases for you to cover:

1. What paperwork to secure?

- Every person born in the US needs a birth certificate and a Social Security number

- Both can be easily applied for at birth in the hospital, by completing a birth registration form and working with the hospital to secure a birth certificate and a Social Security number

- In case of deliveries outside the hospital, you can file for these forms through your local county public health department

2. Why and how to update my beneficiary designations?

- Make sure to update your beneficiary designations in all relevant accounts (e.g., insurance, retirement and investment accounts)

- This allows these assets to speedily flow to the intended recipients, without a potentially lengthy probate process when you pass

3. What insurance to consider?

- Health Insurance:

- Make sure to add your child to your healthcare plan; oftentimes you have 30 days to do so

- Should you miss that special enrollment window, you may have to wait until the next open enrollment season

- Now that your family has grown, make sure to reflect on the optimal deductible amount, coinsurance, and max out-of-pocket levels

- Life Insurance:

- First, revisit or consider starting life insurance for both parents, regardless of whether they work outside the home. This ensures that their income or contributions to the household can be replaced in the event of an untimely death. Explore both term- and whole-life insurance options

- Secondly, consider taking out a policy on your newborn, which may lock in lower premiums well into the future and guard against potential future health issues that may make them uninsurable

- Learn more at https://www.forbes.com/advisor/life-insurance/life-insurance-calculator/ or https://www.bankrate.com/insurance/life-insurance/life-insurance-calculator/

- Disability Insurance:

- Review and potentially add to your short- and long-term disability policies to replace typically 70-80% of your income should you become disabled

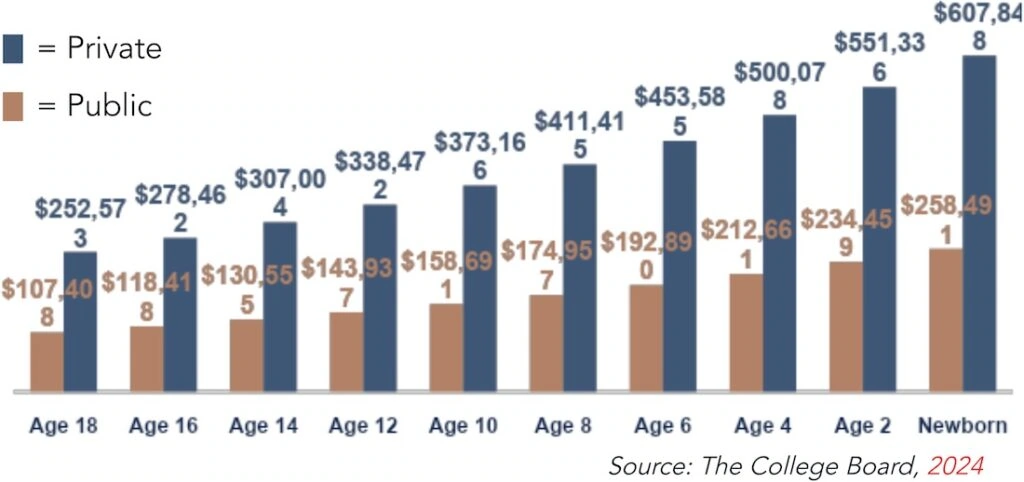

4. What can college cost?

- For the 2024-25 academic year, the average annual cost for tuition, fees, room and board was ~$25,000 for in-state public and ~$58,600 for private colleges (The College Board, 2024)

- Assuming 5% annual College cost inflation, the 4-year cost differs by age of the child:

What are key college financing options to consider?

- 29, UTMA/UGMA and Coverdell Accounts – Contribute and save in tax-advantaged funding sources; learn more at https://www.savingforcollege.com/compare_savings_options/

- To note, SECURE2.0 now allows for up to $35,000 in unused 529 funds to be converted into Roth IRA accounts under certain circumstances

- Pay-As-You-Go – Some families can simply cover college costs out of the annual budget as they go along

- Prepaid Tuition Plans – Some states and private colleges offer pre-payment options; learn more at https://www.savingforcollege.com/article/prepaid-tuition-plans and www.collegewell.com/private-college-529-plan/

- Student Loans – Often a measure of last resort; total US student debt has exceeded $1.7T, with average balances around $40,000 per borrower (Federal Reserve, US Dept. of Education); learn more at https://www.savingforcollege.com/student-loans

- Financial Aid / Grants & Scholarships – Besides colleges, the federal government, states, and non-profit organizations provide numerous forms of grants and scholarships that generally do not have to be repaid. Note, grants are typically need-based, while scholarships are typically merit-based; learn more at https://www.bankrate.com/loans/student-loans/guide-to-college-scholarships-and-grants/ and https://www.usnews.com/education/best-colleges/paying-for-college/articles/an-ultimate-guide-to-understanding-college-financial-aid

5. Why consider Retirement Savings now?

- Continue to take care of your personal retirement savings, so that you do not become a burden to your kids later in life

- Continue to or start taking advantage of any employer-matching 401(k) programs, which are “free money,” and continue to maximize your contributions to tax-advantaged retirement savings accounts

6. What Trust & Estate documents to complete or refine?

- The birth of a child is an excellent occasion to either establish or update several key documents, ideally notarized, including:

- Wills & Guardianships: Provide a plan for the division of your assets, and designate a legal guardian to take care of your child(ren) should you pass prematurely; a properly-executed Will can help avoid your estate going through lengthy probate in the legal system

- Advance Directive for Healthcare: Consists of two crucial documents: a “Living Will” that specifies your wishes for end-of-life care, and a Healthcare Power of Attorney that appoints someone to make healthcare decisions should you not be able to do so

- Durable Financial Power of Attorney (DFPA): Appoint an agent to manage your finances for you should you ever become unable to do so yourself

- Trust & Estate Plan: Explore potential wealth protection and transfer opportunities with your financial professional and legal advisor

7. Any tax opportunities?

- Be sure your tax preparer is aware that you have a new child, as this may affect the number of dependents you can claim on your income tax return, the Child Tax Credit for which you may be eligible, and the Earned Income Tax Credit limitation that apply to you

- Up to $5,000 from a 401(k) or IRA may be withdrawn from a 401(k) or IRA to meet expenses within 1 year of your child’s birth. You will have to pay income tax on the withdrawal, but not the 10% penalty that usually applies to early withdrawals from retirement accounts. You can repay these funds at a later date

8. Why contribute to HSAs and DCFSAs?

- HSA – Health Savings Account

- If you utilize a High Deductible Health Plan (HDHP), consider opening and fully funding an HSA (up to $8,550 per family per year for 2025)

- Ideally, invest your pre-tax contributions, and let them compound tax-free for as long as you can, taking them out tax-free for qualifying healthcare expenses

- Learn more in IRS Publication 969 — https://www.irs.gov/forms-pubs/about-publication-969

- DCFSA – Dependent Care Flexible Spending Account

- Often provided through the workplace, let’s you set aside up to $5,000 per year tax-free for qualified childcare expenses

- Learn more in IRS Publication 503 — https://www.irs.gov/forms-pubs/about-publication-503

Supporting Information

Last Reviewed: 01/27/2025

Key Sources and Further Reading

College

- collegeboard.org

- collegeconfidential.com

- finaid.org

- collegedata.com

- savingforcollege.com

- collegesavings.com

- salliemae.com

- educationdata.org

FSAs and HSAs

- https://www.irs.gov/forms-pubs/about-publication-503

- https://www.irs.gov/forms-pubs/about-publication-969

Social Security

Life Insurance

- https://www.forbes.com/advisor/life-insurance/life-insurance-calculator/

- https://www.bankrate.com/insurance/life-insurance/life-insurance-calculator/

- https://www.dfs.ny.gov/consumers/life_insurance

Archford Capital Strategies, LLC (“Archford”) is a Registered Investment Advisor, registered with the U.S. Securities and Exchange Commission (“SEC”). Registration as an investment advisor does not imply a certain level of skill or training. The information presented has been prepared on the basis of publicly available information, internally developed data or other third-party sources. There is no guarantee as to the accuracy, completeness, or reasonableness of the contents contained herein. Archford Capital Strategies, LLC and its affiliates do not provide legal advice. Tax and accounting services are offered through Archford Accounting, LLC, an affiliated entity of Archford Capital Strategies.