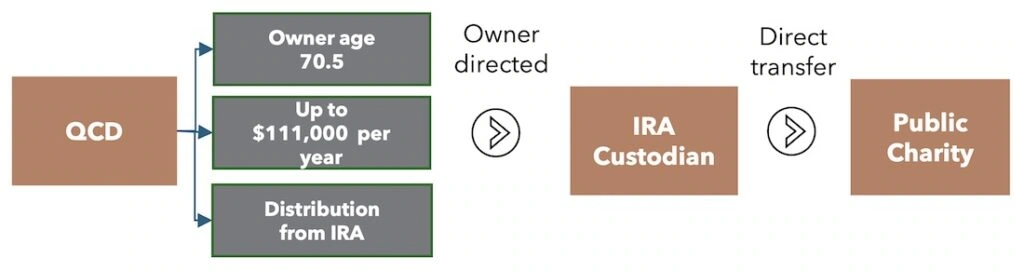

What is a Qualified Charitable Distribution?

- Individuals age 70.5 and older may transfer up to $111,000 per year from their IRA* to a qualified charity without recognizing the distribution as taxable income

- IRA owners aged 73 and older may utilize this strategy to satisfy annual Required Minimum Distributions (RMDs)

* Plans that qualify for QCDs: Traditional IRAs, inherited IRAs, inactive SEP and inactive Simple Plans

Action Steps: How to make a QCD?

- A QCD must be made between institutions; the IRA owner notifies their IRA custodian who then issues a check in the specified amount payable to your selected charity (or charities)

- Individuals may distribute/transfer up to $111,000 from the IRA to charity per year; if the distribution is to count towards the IRA owner’s RMD, this transfer must be made before the December 31 RMD deadline

- Careful: Some charitable entities do not qualify as charitable organizations under this strategy including donor advised funds, private foundations and supporting organizations

Why make a QCD?

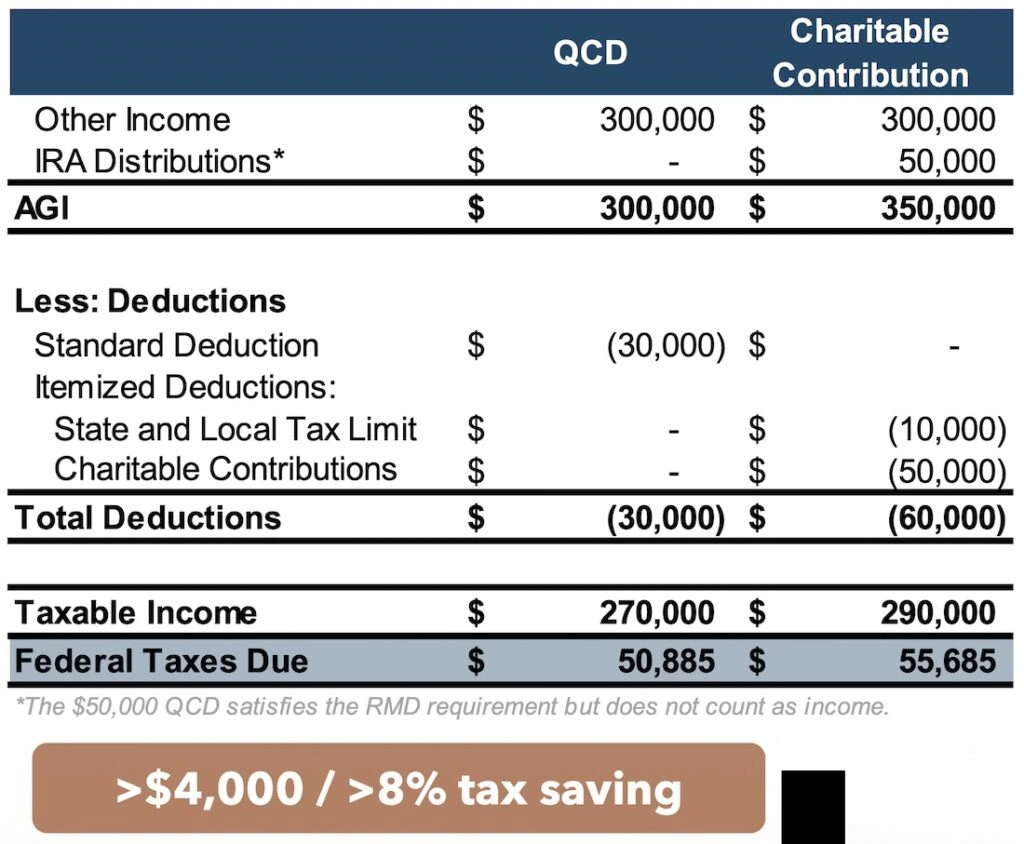

- As of age 73, IRA owners must begin to take annual RMDs which could increase income and taxes

- A QCD can satisfy the RMD requirement while helping a charity and lowering taxes

- A QCD is not a tax deduction but rather an exclusion from your taxable income; this reduces your taxable income and may thus lower your tax burden (see below illustration; focus here on federal taxes only, pre state taxes and FICA)

CASE STUDY

How a Donor Reduced Their Medicare Premiums using QCDs

Jim Maher talks to Frank Pratl about being 70.5 years old and making charitiable donations using his IRA.

By giving through your IRA, a Qualified Charitable Distribution (QCD) will allow you to reduce the income tax owed on your Required Minimum Distribution (RMD). This can reduce your insurance premiums due to a lower adjusted gross income (AGI).

Supporting Information

Last Reviewed: 11/24/2025

Key Sources

- Internal Revenue Code Sections 62, 63, 170, 408, 1411

- Notice 2007-7, 2007-5 I.R.B. 395, IR 2024-289

- IRS Notice 2025-67

Further Reading