Age 65: Get Familiar with Medicare

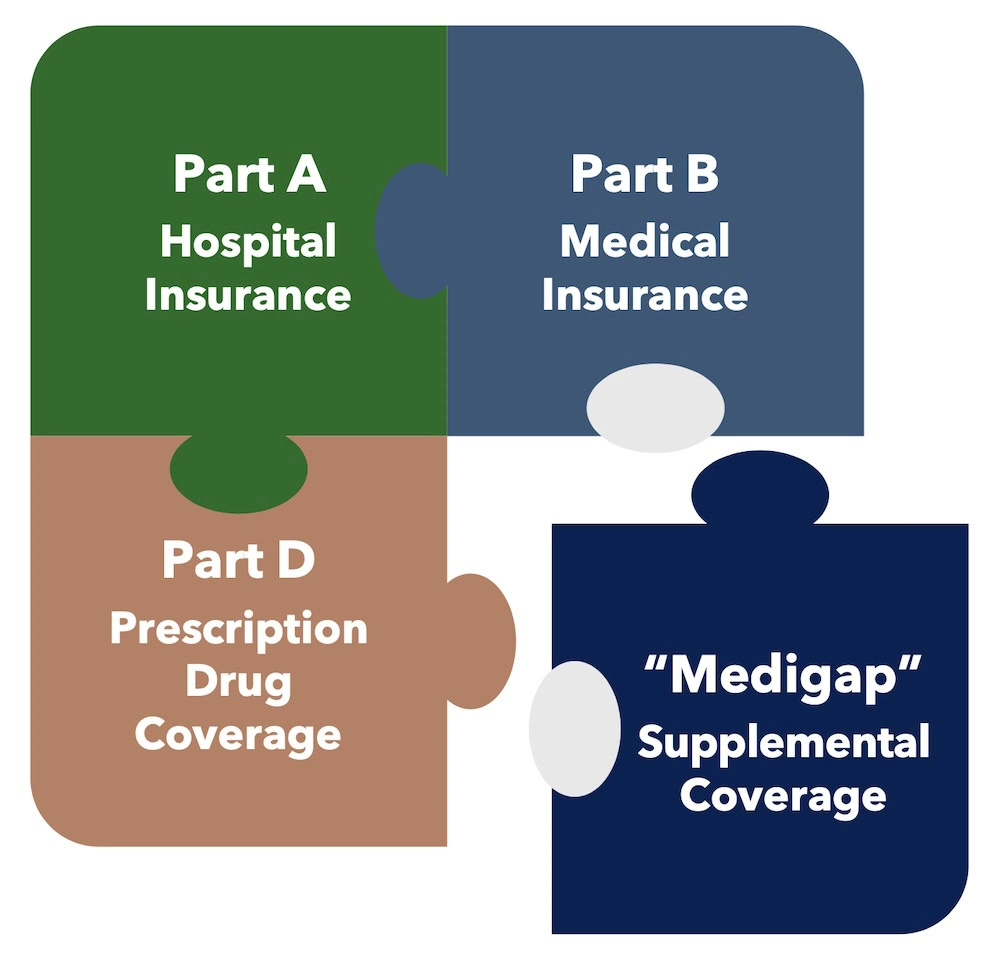

Medicare Has 4 “Parts”

Part A – Hospital Insurance

- Part A covers inpatient care in hospitals, skilled nursing facilities, nursing homes, hospices, and home health care

- Premium-free if you qualify for Social Security benefits or Social Security spousal benefits

- Deductible of $1,736 per benefit period (in 2026)

- Copays for longer hospital stays

Part B – Medical Insurance

- Part B covers medically necessary and preventive outpatient services

- Standard premium is $202.90/month (in 2026); high-income beneficiaries may owe more

- Generally requires you to pay 80% coinsurance, after the $283 deductible (2026) is met

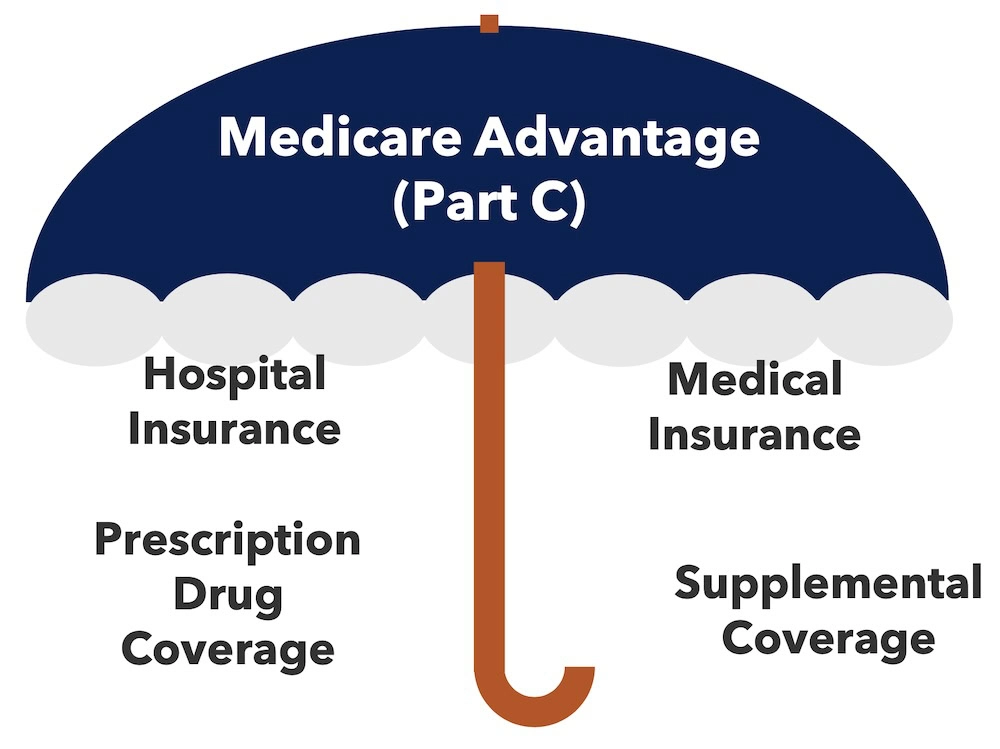

Part C – Medicare Advantage

- Private insurance policies, regulated by Medicare, that are an alternative to the Part A and Part B fee-for-service model

- Covers everything Part A and Part B cover, plus additional services Part A and Part B do not cover, and usually prescription drug coverage (Part D) as well

- Generally operates on an HMO or PPO model, limiting the network of providers you can see

Part D – Prescription Drug Coverage

- Private insurance policies, regulated by Medicare, that provide prescription drug coverage that Part A and Part B do not

- Generally not necessary if enrolled in Medicare Advantage

- Premiums vary by insurer; high-income beneficiaries may owe a surcharge to Medicare

Age 65: How Does Medicare Coverage Fit Together?

Option 1: “Traditional” Medicare

- The “traditional” approach to Medicare combines Part A and Part B, adds Part D for prescription drug coverage, and then usually adds a “medigap” supplement insurance policy to fill gaps in coverage

- Medigap policies are sold by private insurers, but regulated by Medicare

- The “traditional” approach generally does not restrict you to a specific network of doctors

Option 2: Medicare Advantage

- Medicare Advantage is an alternative to “traditional” Medicare whereby you receive your Part A and Part B benefits, usually prescription drug coverage, and other supplemental coverage through the Medicare Advantage policy

- Medicare Advantage generally operates on an HMO or PPO model, meaning you may be limited in the doctors you can see

- However, Medicare Advantage policies often have an annual out-of-pocket spending limit “traditional” Medicare lacks

Age 65: Enroll in Medicare

When do I become eligible to enroll in Medicare?

- Most Americans first become eligible to enroll in Medicare Parts A and B when they turn 65 (individuals with certain disabilities and illnesses may qualify sooner)

- Your Initial Enrollment Period begins three months before the month you turn 65 and ends three months after (seven months total); generally, it is best to enroll in the months prior to your 65th birthday, so your coverage becomes effective on turning 65

- If you do not enroll in Medicare Part B during your Initial Enrollment Period, you may owe late enrollment penalties (10% of your premium for each year you go without coverage)

- If you or a spouse are still working and have health insurance through an employer, you generally will not be subject to late enrollment penalties — instead, you can wait to enroll in Part B during an eight-month Special Enrollment Period after you or your spouse stop working

Action Steps: How to enroll?

- If you are receiving Social Security benefits at the time you turn 65, you will be automatically enrolled in Medicare Part A and Part B

- If you are not automatically enrolled, you can enroll in Medicare online through the website of the Social Security Administration: https://secure.ssa.gov/iClaim/rib

- To enroll in Medicare Part B during a Special Enrollment Period after you retire, you must file Forms CMS-40B and CMS-L564

- Before you can purchase a Part D prescription drug plan, you must have enrolled in Part A or Part B; before you can purchase a Medicare Advantage plan, you must have enrolled in both Part A and Part B; for more information about these plans, visit: www.medicare.gov/plan-compare

- For more information about Medigap policies, visit: www.medicare.gov/medigap-supplemental-insurance-plans

Why begin planning for Medicare now?

- Healthcare is expensive and is something you will generally consume more of as you grow older

- A 2025 study by the Kaiser Family Foundation found that Medicare beneficiaries spent an average of $6,330 out of pocket on premiums and healthcare services per year, up significantly from prior years. For many retirees, these costs represented about 11% of their total income, with lower-income beneficiaries spending an even larger share

- With so many options from which to choose — not just “traditional” Medicare vs. Medicare Advantage, but also employer or other private insurance that may be available to you — you should carefully consider which would work best for you financially

- Of course, what health insurance coverage you need is not just a question of dollars and cents — the types of healthcare services you will need, the doctors from whom you want to receive them, and where you expect to be living when you need them are all crucial factors to consider

- Once you have enrolled in any part of Medicare, you are no longer permitted to make contributions to any Health Savings Accounts (HSAs) you may have. However, HSA funds can still be used tax-free to pay for qualified medical expenses, including Medicare premiums

- As you prepare for Medicare enrollment, be sure to stay in close contact with both your doctors and your financial advisors

Key source: Kaiser Family Foundation, Health Costs Consume a Large Portion of Income for Millions of People with Medicare (April 2025) https://www.kff.org/medicare/health-costs-consume-a-large-portion-3of-income-for-millions-of-people-with-medicare/

Supporting Information

Last Reviewed: 11/25/2025

Key Sources

- 42 U.S.C. Sections 426, 1395, 26 U.S.C Section 368

- www.medicare.gov

Further Reading

- CMS – Enrolling in Medicare Part A and Part B

- CMS – Get Started with Medicare

- SSA – Medicare Benefits

- SSA – Medicare Brochure

Archford Capital Strategies, LLC (“Archford”) is a Registered Investment Advisor, registered with the U.S. Securities and Exchange Commission (“SEC”). Registration as an investment advisor does not imply a certain level of skill or training. The information presented has been prepared on the basis of publicly available information, internally developed data or other third-party sources. There is no guarantee as to the accuracy, completeness, or reasonableness of the contents contained herein. Archford Capital Strategies, LLC and its affiliates do not provide legal advice. Tax and accounting services are offered through Archford Accounting, LLC, an affiliated entity of Archford Capital Strategies.